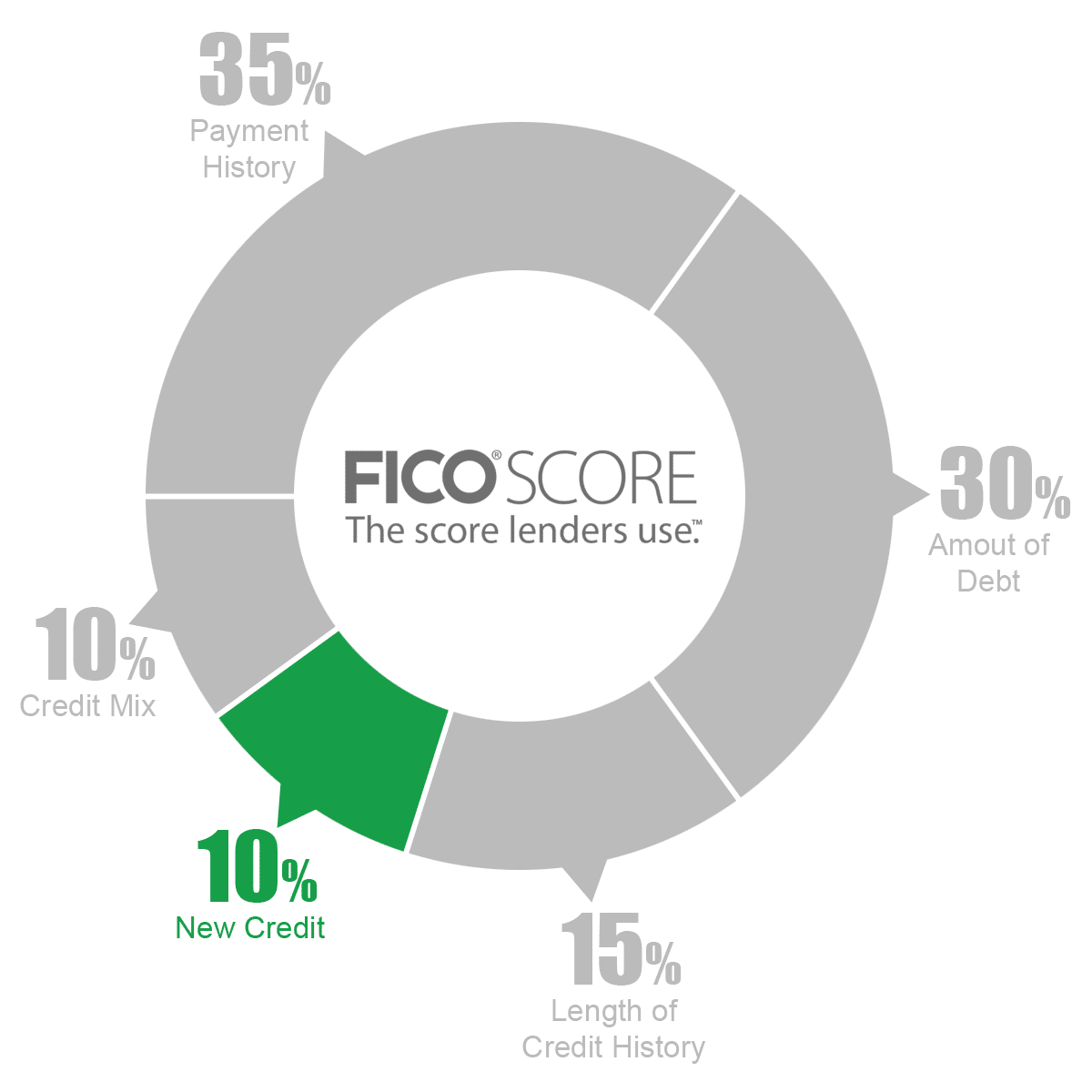

NEW CREDIT & INQUIRIES

10% of Your Credit Score

Several factors are calculated when considering the impact new credit has on your credit scores.

This includes how many new accounts you’ve recently opened and inquiries.

Recently opened accounts consider how many new accounts you have opened up within the last 2 months.

According to FICO, “research shows that opening several credit accounts in a short period of time represents greater risk – especially for people who do not have a long credit history.”

Every time you open a new account your credit scores drop a bit to stop you from establishing too much credit at once.

What does this mean for you?

Establish your credit slowly and don’t panic if your scores drop after you open up a new account, the score will come back up within a few months.

Inquiries

The second part of new credit is inquiries. An inquiry is a record of any company viewing your credit report for the purpose of reviewing your credit history.

The Fair Credit Reporting Act (FCRA) allows any organizations to view your credit file as long as they have a permissible purpose.

There are two different types of inquiries; Hard inquiries, which impact your credit scores, occur when someone checks your credit information for the purpose of obtaining a loan.

A soft inquiry does NOT impact your credit scores.

Too many hard inquiries make a person look desperate for credit and lower their credit scores.

Inquiries Impact on Credit Scores

A hard inquiry can report on your credit for up to 2 years but, according to FICO, only the last 1 year worth of inquiries actually impacts your FICO Credit Scores.

On top of that, inquiries ran within a one-month timeframe, within the same industry, are grouped together and only count against your FICO score as one inquiry.

So if you went car shopping and your auto dealer sent your credit application to 12 different lenders who each ran your credit report – don’t worry.

Although all 12 inquiries will report on your credit history, they will only impact your credit score as a single inquiry.

This is known as rate-shopping.

Can Inquiries Be Removed?

If you have ever disputed inquries with the credit bureaus you know that the probablity of a detion is slim to none.

Most often, the credit bureaus mail you a response stating that, “Inquiries are a matter of record and if you wish to dispute their validity to contact the creditor that pulled your reports directly”.

Inquiries fall under the permissible purpose section of the FCRA which states that every creditor reporting an inquiry on your credit report needs to have a permissible purpose (proper authorization) for the inquiry.

You can request that all of the creditors reporting inquiries provide proof of permissible purpose, if they have the proper authorization, the inquiry will stay, if they can’t verify permissible purpose, the inquiry is deleted.

If you need help.

CreditFirm.net has helped our clients remove thousands of inquiries from their credit reports.

FICO High Achievers

Consumers with FICO scores of 780+

• Opened their most recent account an average of 2 years and 5 months ago.

• Less than 35% of High Achievers applied for new credit once or more in the past year.

Why Choose CreditFirm.net?

Assurance. Our Credit Repair process was developed by experienced attorneys.

Speed. Documents are typically processed and sent out for investigation within 3-5 days.

Support. Award-winning customer service guarantees your satisfaction.